Welcome to The Next Founder

Or why all startups are different but end up having many of the same problems

“Genies are not easily persuaded to return to their bottles, progress is not going away, and change is not going to slow because humanity would like a mental health break.”

— Walter Russell Mead

“If the path before you is clear, you're probably on someone else's.”

― Joseph Campbell

“You must unlearn what you have learned.”

— Yoda, Star Wars: The Empire Strikes Back

Keep your hands and feet inside the ride

You jump out of bed Monday morning and charge down the hall to your new “office” — your kitchen table. You and your co-founder left behind the plump paychecks and posh benefits of your big company jobs and can pursue your startup full-time beginning today. You have no boss and no meetings to distract you, just uninterrupted time, all day, every day, to turn your startup dream into reality.

A month later, you have unwelcome nightmares about quitting. No customer has responded to your LinkedIn meeting requests, you have made glacial progress on your product, you are one month closer to draining your savings account, and the hum of your refrigerator is driving you mad.

A prospect converts their free trial to a paid subscription — your first dollar of revenue! You frame the order form, tack it to your wall, and head into the city with your co-founder to celebrate with burritos and Dos Equis. Your startup is officially legit! Fame and fortune will surely follow.

The next day, a competitor announces $10 million in Series A funding. Your first and only customer calls to tell you they like the competitor’s approach. Your co-founder asks you to go out for drinks for the second time in two days. This time, they have news to break to you: they can only afford to work for free for another month.

You pay an executive search firm a month of your cash to help you hire a VP of Sales. After six months, dozens of interviews, and twelve reference checks, your new VP starts next week!

On Monday, the VP ghosts you. He ignores your calls until the next day when he tells you he had misgivings about your business and took a better offer at a more established company. Now you’ve lost six months, have no other candidates in your pipeline, and have to convince the search firm to redo the search for free.

You open a tiny office in New York City and hire a handful of new team members to take care of your East Coast customers. You are now a bi-coastal company!

The next week, one of your fresh New York hires launches a rant to a coworker about how he hates working with women. You jump onto a red-eye to fly 3000 miles to fire him the next day. He screams at you as you escort him out of the building.

You wake up to an eight-figure wire transfer hitting your bank account from the large public company that just bought your startup. All you have to do is join the BigCo for a couple of years to vest the rest of your stock and mesh your team safely into the cogs of the corporate machine.

Three months later, you are miserable. You spend your hours in endless meetings fighting political battles with BigCo middle managers who want to break up your team and grab your people like they are chopping up a stolen car. You set a timer to count down the days until you are done vesting your stock, after which you can return to your kitchen table to work on your next project, which is, naturally, another startup.

Yeah, this is what it’s like

Over my 30-year startup career, these vignettes have happened to me or to someone I’m close to. They all have one thing in common: they involve your startup’s people. They involve keeping yourself motivated, and productive. They involve keeping your relationship with your co-founders on solid footing. They involve hiring and keeping a great team and building a great culture.

When you spend time with startup founders, you won’t hear tales of launch parties, podcasts, and conference keynotes. You won’t hear about a killer software design someone came up with or a clever sales pitch that won a deal. They’ll spend most of their time talking about the people. You’ll hear about co-founder conflict. You’ll hear about months spent on an executive search that went nowhere. You’ll hear about the key employee who stopped answering their email a month ago.

If you start or join a startup, you’ll write your own stories, but they’ll echo these. You’ll swing between moments of elation when your team is firing on all cylinders and starting to fulfill your vision and moments of doom where no one is getting along and you stay awake all night worried that you are going out of business, probably because you might.

You can see my full biography at My Story. The summary is that I’ve been a founder or the first employee at five startups and have invested in or advised about 50 more. I’ve been through an IPO, on both sides of several acquisitions, on the executive teams of two public companies, and I ran one startup into the ground. I’ve been a CEO, General Manager, Chief Product Officer, VP of Engineering, CTO, VP of Customer Success, board member, advisor, and investor.

I’ve helped raise over half a billion dollars, have hired a few thousand people, and have let go or laid off a few hundred more. I’ve sat through a thousand executive team meetings, several hundred board meetings, and thousands of one-on-ones and staff meetings. I’ve given a few dozen conference keynotes, lectured at Stanford, Harvard, and ESADE, written 2,000 Quora answers, and was nominated for a Webby (yeah, that was a thing for a hot moment).

The gap between theory and reality

In short, I’m really into startups. At their best, they can provide extraordinary careers, build new wealth, and bring much-needed new products and services into the world. But most startups never create much impact, and the root cause can usually be found within the founders and the teams they create. They hit several problems:

The founders are inexperienced

People who start or join early-stage startups are rarely polished corporate executives with expensive MBAs and years climbing the ladder at large corporations like GE or IBM. They are more likely to be a ragged bunch of misfits early in their career, sometimes straight out of school or even dropouts. Many are engineers, designers, or researchers with little experience in “the business stuff” like sales, marketing, and finance.

The founders have the wrong experience

Founders who do have experience at larger companies can have the opposite problem: that experience hurts them as much as it helps them. Lessons learned from selling a mature product to an established market don’t apply to startups. Those founders can flail for a few years as they realize that what worked at Merck or McKinsey doesn’t help a three-person company with no brand and no customers.

The founders are human

As brilliant and determined as many founders are, they have the same mental barriers, emotional roadblocks, and conceptual biases as the rest of us. They dismiss bad news, delay hard decisions, and avoid difficult conversations. The stress of the startup triggers anxiety, imposter syndrome, or burnout. Some let their ego prevent them from responding to feedback. Some ignore the wealth of useful startup advice now available, or they go too far the other way, endlessly reading books and blogs looking for the “right answer” as a way to delay making decisions.

The founders hit a ceiling

Even when a startup does manage to build a good team and get some customers, it can still fail when the business grows faster than the founders’ skills. They might struggle to hire after exhausting their immediate network. They make bad hires and are slow to replace them. They can’t train new sales reps to pitch the product as successfully as the founders could. They find themselves racing their own startup, trying to learn new skills just before they are needed, like they are laying down tracks ahead of a moving train.1

The founders are working on the wrong thing

Founders love their ideas, but they have to pick the right one, and they have to be open to their ideas being challenged.

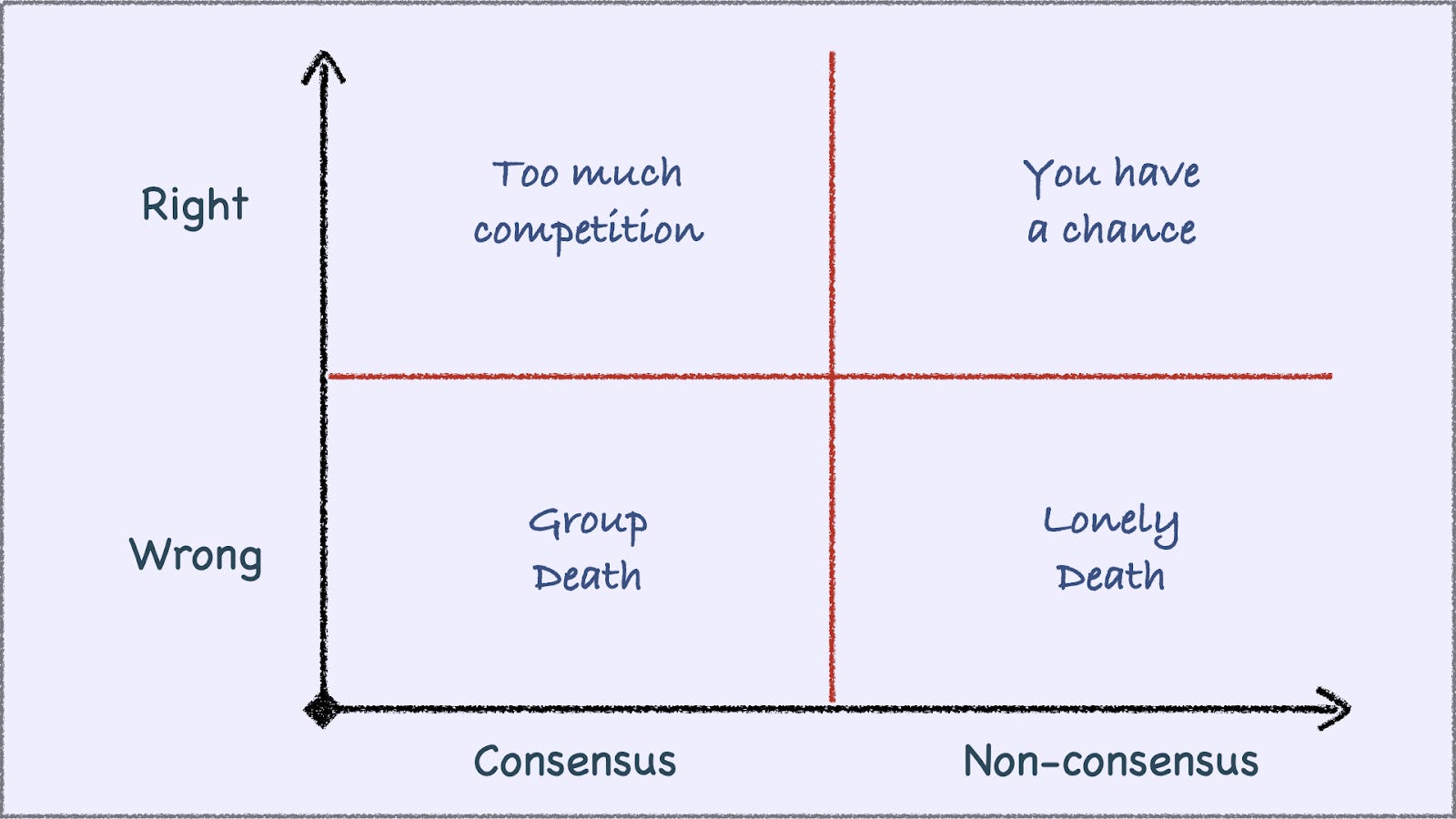

Every startup has a core belief, or ''hypothesis,” about a market, a problem that market has, and a solution for that problem. Few people can reliably predict the market’s reaction — if it were obvious, it would have already been done. You never know if the dogs will eat the dog food.

If your hypothesis is wrong, you won’t get anywhere unless you pivot to one that’s right. But even if you are right, you’ll probably still fail if the hypothesis is too obvious, since obvious ideas attract too much competition. Investors and founders call this “non-consensus and right.”2

Non-consensus is why so many startup ideas seem ridiculous at first. Would you have invested in “let strangers sleep in your spare bedroom,” “the world’s 20th search engine,” or “upload your source code to the cloud?”

The best founders have a knack for finding these non-consensus ideas or pivoting to one that is.

The founders don’t found anything

The main reason a startup “fails” is that it is never started. True, most people should not start a startup, but the number of potentially great founders who don’t take the leap must far exceed the ones who do. They may not know credible founder role models, advisors, or investors. They may live somewhere with a social stigma against working for a tiny, unknown company rather than landing a coveted big company or government job. Or they may not work up the nerve to take such a massive leap into the unknown.

Next Founder’s mission is to help close these gaps. We need more successful startups, so we need more great founders willing to start them, need more of those startups to succeed, and we want anyone who starts or works at a startup to have such a great experience that they can’t wait to do it again.

Most importantly, we explore the gap between knowing the right thing to do and doing it. I can’t tell you if you should fire your VP of Marketing, but I can tell you that you’ll wait way too long to do it, lose sleep over it, and delude yourself that maybe he’ll improve with just a little bit more time (he won’t).

What Next Founder does not cover

Let’s start with what we won’t cover:

The secret playbook

When an intelligent person asks an interesting question, the answer is, “It depends.” It depends on the people, the market, the product, and the timing. Every decision comes with tradeoffs and compromises. No playbook, checklist, or recipe guarantees success, or else we’d all be billionaires.

“It depends” is not a great way to get subscribers, but that’s not my goal. We are happy to wallow in the gray areas, helping you absorb the firehose of advice coming at you, extract the deeper principles that underlie it, and then use them to carve a path to success that works for you.

Fundraising

Startup fundraising has been covered to death, partially because so many venture capitalists crank out content to build their brands. You can find hundreds of blog posts, sample pitch decks, demo day videos, and books on how to raise funding for a startup. I won’t toss more onto that teetering pile.3

I don’t cover fundraising for a more basic reason, though: it’s less important than you think. Founders usually think their idea is so good that their only barrier is money. They think that once the funding rolls in, they’ll hire some engineers and build their product, and it will fly off the shelves. This almost never happens. Founders who raise money from good investors fail all of the time, usually because of problems that money couldn’t have solved.

Regardless, the best way to raise funding is to build something worth funding: a compelling team building a great business. Once you’re on the path to doing that, you can easily learn how to connect with investors and share your story with them.

How to get ideas

A great startup seldom happens because a would-be founder woke up one day, decided a startup would be cool, brainstormed some ideas on a whiteboard, and picked the most plausible one. “Whiteboard ideas” are usually picked over, generic, and obvious, managing to be both consensus and wrong.4 The founders who pursue them seldom have unique insight into the problem or passion for solving it.

The best startups come from a compelling set of founders who lived a set of experiences that gave them insight into a market and a problem that market had. They start a company to get a solution into the hands of those customers.

You hopefully already know the startup you are building and are looking for help to build it better and faster. If you don’t, this can motivate you to find that idea and give you a preview of your life once you do. We’ll also help you learn why you need to be “all in'' on your idea; startups are so hard that you probably won’t stick with yours for long if you don’t find an idea you want to live and breathe for a decade.

Functional advice

Next Founder won’t discuss how to design a sales compensation plan, A/B test your landing pages, compute your net dollar retention, or shepherd a drug through clinical trials. We’ll focus on the more universal and timeless problems all founders have, regardless of whether they work in software, biotech, cleantech, or consumer businesses.

What Next Founder does cover

Each chapter of Next Founder covers an aspect of managing yourself or your team. We’ll publish a new one about twice a month. Each chapter includes:

Vignettes

We start with a vignette about founders facing typical challenges and opportunities with themselves or their team. These stories are “truthy” in that they are inspired by real stories or at least mash-ups of them. Many start with our founder heroes lying awake at night, agonizing over a tough dilemma. You might find these fictional founders to be a bit neurotic, nothing like the decisive and steadfast leader you plan to be. To this, I say: just you wait.

Counterintuitive advice

Startups don’t always make sense, and you can’t always rely on your instincts. Founders need to forget much of what they think they know about business, especially lessons learned at larger companies. We’ll talk about leaving your comfort zones, risking failure, staying agile, and living with ambiguity and chaos.

Core principles

Instead of stopping at superficial advice like “hire good people” and “be authentic,” we dig deeper and asks what lower-level principles underlie that advice and what tradeoffs and compromises that advice entails. Great founders learn to make people decisions that balance the upsides and the drawbacks.

Great resources

Many successful startup founders and investors are also the best thinkers and writers in the industry. They’ve produced fantastic blog posts, books, videos, and classes. Next Founder links to the best from investors like Paul Graham, YCombinator, and First Round Capital, from founders like Naval Ravikant, as well as more classic sources of business advice like Michael Porter, April Dunford, and Geoffrey Moore.

A startup doesn’t happen unless you start it, so let’s start by talking about the only thing a founder can do: Start Where You Are.

Once you watch this video of Gromit laying tracks in front of a moving train, it will pop into your head daily. You can thank me later: Gromit Placing Rail Tracks for 10 Hours.

I first heard “non-consensus and right” from legendary Benchmark Capital investor and Stanford Business School lecturer Andy Rachleff. Peter Thiel refers to a similar concept in “Zero to One” when he discusses the “secrets” of great founders.

When it comes time to raise money, you’ll want to read Venture Hacks, Venture Deals, much of the content from YCombinator, and sample pitch decks and critiques of them. Just please don’t watch “Shark Tank.”

Paul Graham’s “How to Get Startup Ideas” is the best writing I’ve found on where founders get their ideas. One of the conclusions might be discouraging: the best ideas often happen when the founders aren’t even looking for them.

Also, check out the Stanford courses “CS183: Startup” (Peter Thiel) and “How to Start a Startup” (Sam Altman). Read SaaStr, especially if you are a B2B startup. Read the Marc Andreessen blog series and the entire series of essays from Paul Graham.

That was a great story and advise. Thanks for Sharing!

Good post! I think this will be a rich vein for founders to absorb and live by!