7. Grasp Why You Get Paid

7. Grasp Why You Get Paid

Or why, if you make it big, it won’t be for the reasons you think

Uninvent is designed to help startup founders build successful companies and stay healthy and sane while doing it. Please see the overview in Welcome to Uninvent and links to past and future chapters in Uninvent Table of Contents.

“It is not enough that we do our best; sometimes we must do what is required.”

― Sir Winston Churchill

“If you're in a job that feels safe, you are not going to get rich because if there is no danger, there is almost certainly no leverage.”1

— Paul Graham

“It’s not really about hard work. You can work in a restaurant for eighty hours a week, and you’re not going to get rich. Getting rich is about knowing what to do, who to do it with, and when to do it. It is much more about understanding than purely hard work. Yes, hard work matters, and you can’t skimp on it. But it has to be directed in the right way.”2

— Naval Ravikant

Like running in sand

The first year of your startup was a slog, and the stress dream is back: the one where you are running in deep sand while being chased by a pack of mountain lions. You don’t need Freud to explain this one: your startup is going nowhere.

Only a few customers use your product. Some have given you an idea for a pivot, but you are reluctant to put it into motion. For months, you’ve urged your team and investors to be patient and keep the faith. A pivot means going back to them with, “Whoops, forget everything I said before, but listen to me starting now.”

On top of that, your Director of Engineering is a problem. He’s a mediocre performer and is partially responsible for your predicament. Firing him will be painful since he’s a hard worker, and the team likes him. You keep finding ways to delay the tough conversation you need to have with him, using the potential pivot as an excuse to do nothing.

You have several unanswered “we need to talk” Slacks from team members. You don’t expect them to age gracefully, but you know they’ll be energy-sucking conversations about questions you don’t have answers to. You hide in your office, rationalizing that you need “thinking time.”

Coding always relaxes you, so you start fixing bugs in your product so that you can at least achieve something today. You leave the office close to midnight, exhausted, wondering if feeling this stuck is normal.

Yes, it is normal to feel stuck, but it’s also normal to fail. You might be able to turn it around, though, if you grasp why you get paid.

The price of success

A startup founder can make a pile of money. Thousands of founders and early startup employees have walked away from startups with seven-, eight-, and even nine-figure fortunes. Over 100 members of the Forbes Billionaires list landed there by starting a tech startup, often in their 20s and 30s.3

On top of the cash, successful founders enjoy the camaraderie and respect that come from building a winning team. They relish the ego boost of speaking at a conference or their high school commencement. Most of all, they get the satisfaction of building something that helps their customers and changes the world in at least a small way. These payoffs are why, after a win, so many founders start another startup and invest in other startups.

Who gets rich and who doesn’t might feel disquieting and even unfair, though. Why do so many promising founders go nowhere while seemingly less talented ones walk away loaded? Do you deserve to earn a hundred times more than your barista or even your doctor? Where does the money come from, and how do you know if you’re working on things that bring it your way?

If you learn the answers to these questions, you are not only more likely to succeed, but you may also retain a bit of humility if you do. You don’t want to be a failed founder, but it’s not much better to be a successful but insufferable one.

Let’s talk about how you get paid.

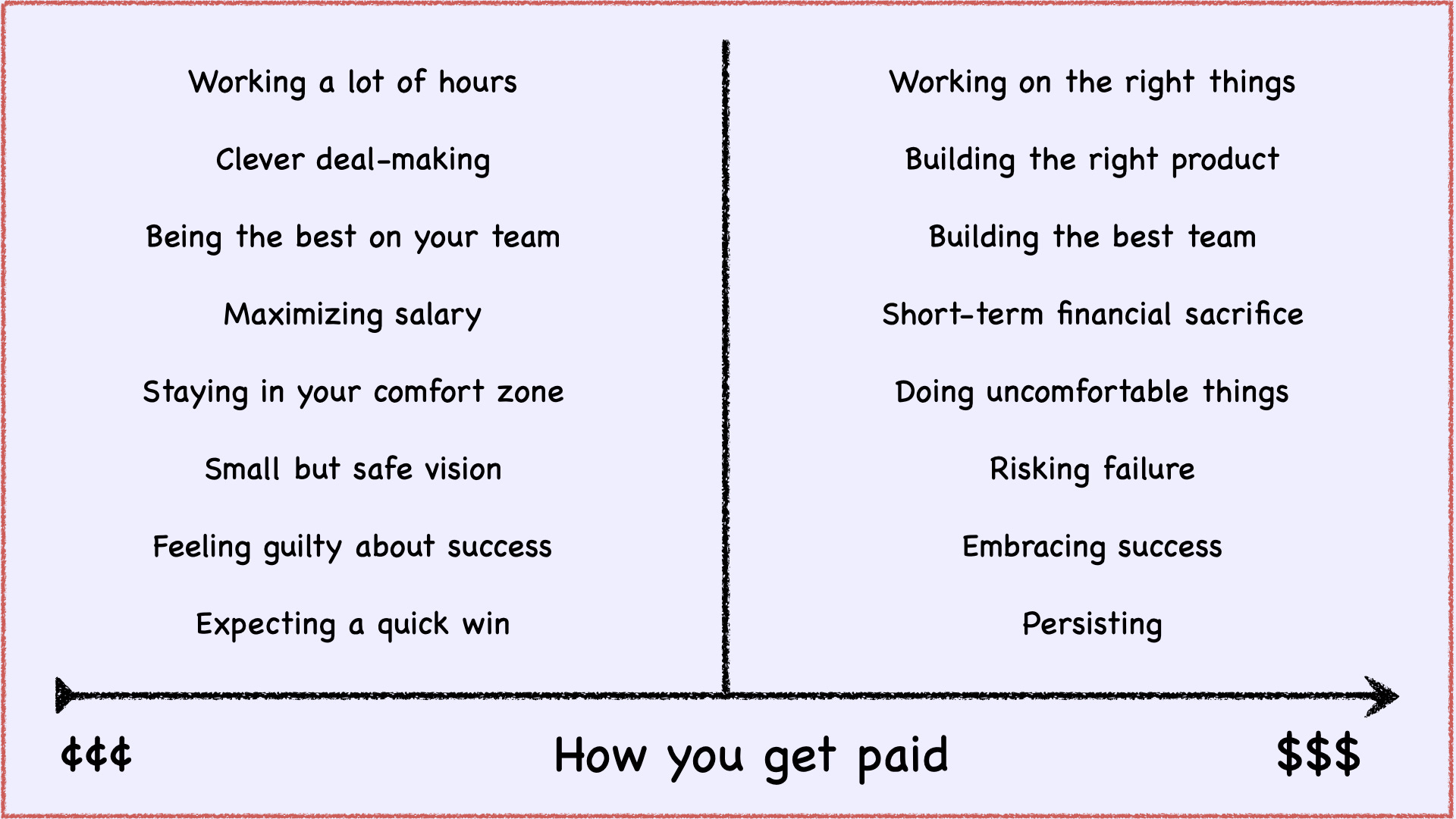

You get paid for your output, not your input

As a startup founder, you’ll work harder than at most other jobs and harder than most people who work for you, but working a lot of hours isn’t why you get paid. No one has more than 60–80 productive hours per week in them. Mark Zuckerberg didn’t become a billionaire by working 10,000 hours per week. And you aren’t working harder than the single mom next door, who holds down two jobs.

The hours don’t matter unless you are working on the right things. You don’t get paid for building the wrong product, hiring the wrong people, or for executing a go-to-market strategy that doesn’t connect with your buyers. You may as well be driving a car 100mph down the highway in the wrong direction. The wind whipping through your hair gives the illusion that you are moving toward your goal, but you’ll finish further from success than when you started.

You also don't get paid for work that is easy and in your comfort zone. The right work usually isn’t. Firing someone is uncomfortable. Cold calling a hundred prospects when you’d rather be coding is difficult. Pivoting your idea because your product isn’t selling is risky. But you get paid for doing the work that needs to be done, not for the work you feel like doing.

The world is indifferent to your hard work and sacrifice. You have no boss to impress or professors to give you extra credit. All that matters is what you produce for your customers.

You don’t get paid for being the smartest

Brainpower is crucial at a startup, and most founders have plenty of it. Use it if you have it, but don’t expect to get paid for being the smartest person on your team.

A founder who wants to be the smartest person in the room can make it a self-fulfilling prophecy by filling the room with less talented people. They hire a team that won’t outshine or challenge them, but that’s a path to mediocrity.

Your job is the opposite: hire the best people you can, spend time training them, and ask them to leave when they aren’t working out. You won’t get the ego boost of always being the one with the answers, but you might get paid.

You get paid for risking failure

Most startups fail, and their founders can work for years with little financial success to show for it. The high failure rate makes sense—if startups were guaranteed cash, everyone would start one. Fear of failure can be even worse than the failure itself, as founders lay awake at night, envisioning going broke and being shunned as a loser by friends and family.

The good news is that you aren’t risking your life. You aren’t serving a tour in Iraq or dodging heavy machinery in a coal mine. You are sitting in front of a Macbook, sipping a latte. Yes, the stakes are high, and what you are doing is important, but if you fail, you’ll live to see another day, and you‘ll have new skills and a great network to leverage into your next gig.

You don’t get paid for elbowing people out

Many industries are zero-sum games where only a handful of people can win. If you were a basketball player trying to make an NBA roster or an aspiring actor trying to break into Hollywood, you’d have to beat out thousands of other hopefuls vying for a handful of coveted spots.

Startups don’t work like this since there is no practical limit to the number that can succeed. To build a winning startup, you only have to beat a handful of direct competitors in your market. Anyone else you meet, whether it’s another founder, an investor, or a recruit, is someone to work with or to learn from. This is why the tech industry is so collaborative. It’s a positive-sum game. Helping someone else win doesn’t mean you’ll lose.

Some founders mistakenly assume startups are like other industries, where powerful gatekeepers decide who gets a shot and who doesn’t, so venture capitalists must be those gatekeepers. Popular entertainment like “Shark Tank” bolsters this fallacy, portraying investors as if they were movie producers who pick the winners and losers out of the lineup of fresh-faced supplicants waiting in line at their door.

The truth is less interesting. There are thousands of investors who want to put money to work, and most will tell you they wish they saw more great startups. Yes, investors have biases and blind spots like anyone else, but they are all looking for the same thing: a startup that might turn into a big company because it’s tackling a great market with a fantastic team. If you have one, you have a good chance of raising money if you need it.

You get paid for building a product that customers need

Some founders assume they get paid for dazzling a VC into writing a check or launching a clever marketing campaign to wow customers into parting with their money. And yes, deal-making is an essential skill for a founder. But you don’t get paid for wheeling and dealing; you get paid for having a product worth wheeling and dealing over.

Nothing happens at a startup until you build a product that customers love, collect their money, and convince them to sing your praises. Raising money doesn't help if you don’t use it to build a great product and get it into customers' hands. An excellent distribution strategy doesn’t matter if people don’t want the product in the first place. Even hiring great people doesn’t matter if they aren’t building and selling a product that people want.4

Product/market fit doesn’t guarantee you’ll build a big company, but not having it guarantees you won’t.

You get paid for financial sacrifice

Many founders work with little or no pay. Even after they generate some revenue or obtain funding, they take salaries below what they could get elsewhere. If their equity doesn’t end up being worth much, they exit the startup years later poorer than if they had spent the time doing something more lucrative.

The required financial sacrifice can be unfair. Some founders have rich friends and family who can provide seed funding, but most don’t. Some have family responsibilities that require them to maximize their short-term income. Many founders have overcome these roadblocks, but overcome them, they must.

The sacrifice varies by founder. For a Harvard MBA who would otherwise be making $500K at an investment bank, a startup represents a huge opportunity cost. For a high school dropout whose alternative is a more ordinary job, the startup wouldn’t represent much sacrifice at all. This is why founders without a great Plan B are some of the most persistent; they are less tempted to quit. And it’s why so many elite college graduates’ interest in startups doesn’t survive first contact with the canapés at Goldman Sachs career night.

You get paid for wanting to get paid

The first glimpse of success can disorient a founder. A founder who owns 40% of a startup that raises a series A at a $30 million valuation wakes up with a theoretical $12 million net worth on paper, which generates a cocktail of emotions, including fear of losing the money and guilt for having it.

Don’t worry about it. If you are getting rich, your employees are, too. It means your investors will get a return, which goes to the pension funds and endowments that make up the bulk of the capital they invest. It means your customers are buying from a company that will stay in business.

If your wealth ever becomes liquid, you’ll pay a lot of taxes, and you can donate to causes you value and invest in the next generation of startups. Don’t lose any sleep. It’s fine.

You get paid for persisting

A new startup is like a baby: a perfect little being with no flaws and infinite potential. Not long after it's brought into the world, its owners find themselves awake at 3 am, wearing the same vomit-covered clothes they wore yesterday, wondering if it’s ever going to get easier.

A startup usually takes off slower than its founders expect, if it takes off at all. If the slowness is because the startup is working on the wrong idea, the founders need to pivot or quit, but even successful startups can take a decade to grow to a substantial size. Much of the growth happens in the latter years due to the magic of compounding.5 A startup might take a decade to reach a $500 million valuation but hit $1 billion just a couple of years later. Founders get paid for spending years of their lives plugging away making this happen.

Founders who burn out or let their physical or emotional health atrophy are useless to their startups, so taking care of yourself is part of your job, not only for your own good but also for the good of your team. This means focusing on sleep, exercise, diet, and maintaining social and family connections.

Yes, you’ll make sacrifices, but make the ones that produce results. Don’t make them just for the sake of making them. Don’t miss your friend’s bachelorette party because you think the startup gods will punish you for taking a couple of days off.

We’ll cover many of these topics in more depth in future chapters, starting with Be a Learn it All.

Paul Graham’s essay “How to Make Wealth” is another one of his must-reads.

AngelList founder Naval Ravikant is an absolute font of advice on startups and wealth creation. Eric Jorgenson summarizes Naval’s work in “The Almanack of Naval Ravikant.”

The Forbes Billionaire List is now updated in real-time, in case you need extra motivation.

Marc Andreessen’s original essay on product market fit is still the best thing written on the topic. You’ve probably also heard the YCombinator motto, “Make something people want,” which may seem like obvious advice, but if it were, they wouldn’t have to repeat it so often.

Albert Einstein said, “Compound interest is the eighth wonder of the world.” Compounding doesn’t just apply to money sitting in an account. It also applies the investments of time, effort, and talent into a startup.